How Blockchain Technology is Redefining Trust in Digital Transactions

Blockchain technology is revolutionizing the way we approach trust in digital transactions by providing an immutable and transparent ledger system. Traditional transaction methods often rely on centralized authorities, which can lead to potential fraud, data breaches, and a lack of accountability. With blockchain, every transaction is recorded in a decentralized manner, making it nearly impossible for any single entity to alter or manipulate the data. This shift not only enhances security but also fosters greater trust among users, as they have access to a comprehensive history of all transactions on the network.

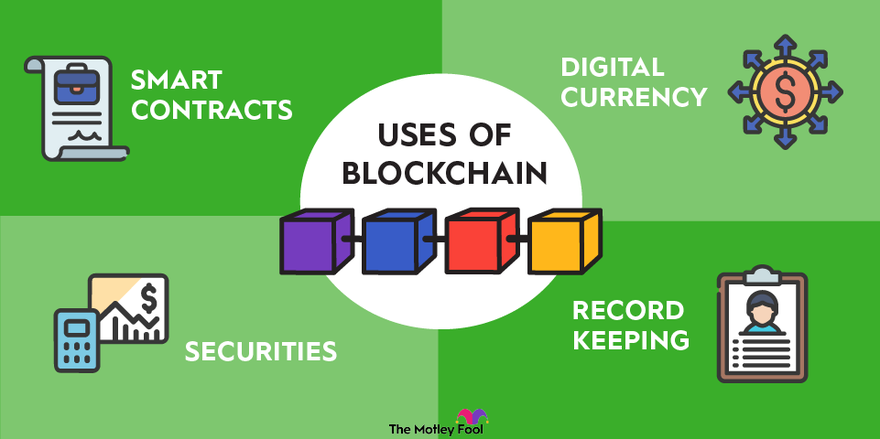

Moreover, the decentralized nature of blockchain encourages innovation in various sectors, such as finance, supply chain, and healthcare. By eliminating the need for intermediaries, blockchain technology streamlines processes and reduces costs, ultimately benefiting both businesses and consumers. The implementation of smart contracts further strengthens this trust by automating agreements and ensuring compliance without the need for human intervention. As more organizations adopt these technologies, the paradigm of trust in digital transactions is being fundamentally transformed, leading to a more reliable and efficient digital economy.

The Challenges of Trust: Understanding the Limitations of Blockchain

While blockchain technology is often hailed for its decentralized nature and ability to enhance trust, it is essential to recognize the limitations of blockchain that can pose significant challenges. One primary issue is scalability. As more transactions are added to the blockchain, the system can experience slowdowns, making it difficult for the network to process a high volume of transactions efficiently. This can lead to longer confirmation times and increased transaction fees, which can undermine the trust users place in the technology.

Another challenge lies in the security vulnerabilities associated with blockchain networks. Though the technology is designed to be secure, it is not immune to attacks. For instance, a 51% attack can occur when a single entity gains control of the majority of the network's hashing power, allowing them to manipulate transactions. Additionally, the trust in blockchain can be compromised by human errors, such as poor key management or flawed smart contracts, highlighting the necessity for a deeper understanding of the intrinsic risks involved in adopting this otherwise revolutionary technology.

Can Blockchain Truly Solve Trust Issues in Today’s Digital Economy?

In today's rapidly evolving digital economy, trust issues continue to plague interactions between consumers and businesses. Traditional systems often rely on centralized authorities, which can lead to a myriad of problems, such as fraud, data breaches, and lack of transparency. Blockchain technology emerges as a formidable solution by providing a decentralized and tamper-proof ledger that enhances transparency and accountability. With its ability to securely record transactions without the need for intermediaries, blockchain holds the potential to foster greater confidence among users, thus reshaping the landscape of trust in digital transactions.

Moreover, the decentralization offered by blockchain can effectively bridge the trust gap in various sectors, including finance, supply chain management, and digital identity verification. By enabling participants to verify transactions independently, blockchain mitigates the risks associated with fraudulent activities. For instance, in supply chains, all parties can trace products back to their origin, ensuring authenticity and ethical sourcing. As businesses increasingly adopt this transformative technology, the digital economy may well become a more trustworthy environment for all stakeholders involved.